Just like the job of the Fleet Manager has transformed into that of a Mobility Manager, the car policy is evolving towards a mobility policy. Corporate mobility has become much more than just providing cars or LCVs – it’s about organising individual and shared transport in all its shapes, with people, planet and profit as key drivers.

In today’s corporate mobility policy, Mobility as a Service (MaaS) plays a touchstone role. But how should you build a MaaS strategy that motivates your employees to get the most out of all the mobility options that it provides? Like most strategies, a step-by-step approach is probably the best practice.

1. Understand your current status

Inventorize the mobility needs that exist within your company. This is dependent on your company’s location, your employees’ commutes, and their business mobility needs.

2. Identify stakeholders

Human Resources, Finance, Procurement, Facility Management, Sustainability,… the list of corporate departments with an interest in corporate mobility seems to get longer every year. It’s important to identify who they are in your case, and how MaaS can benefit their specific strategy – in other words: find out “what’s in it for them”.

3. Go to the market

Depending on where you are, the mobility solutions on offer may range from fairly narrow to relatively broad. Within those restrictions, find the suppliers whose mobility offers best fit your need.

4. Test and validate

And which ones best fit your need? The best way to find that out is to test them. Seek out motivated drivers to set up pilots. This will help you validate what works (and why, and to which degree).

5. Implement at an appropriate level

The MaaS landscape is still very fragmented. Mobility providers typically operate locally – often in specific cities rather than entire countries. That means pilots (and eventual mature MaaS programmes) may have a very limited geographic scope.

6. Follow up and develop

MaaS is an industry in constant flux and perpetual development. Today’s limits may have moved by tomorrow. Keep adapting your MaaS strategy to what’s on offer – because it will evolve all the time.

7. Don’t wait for perfect

Universal MaaS – all solutions available everywhere – is so far away that it may never happen. But don’t let ‘best’ be the enemy of ‘better’. Accept that the perfect MaaS solution may never arrive. Work with the improvement that the MaaS solutions that do exist can offer you.

Uncertainty is what characterises business life in the New Normal, but cost-cutting is bound to be the main priority of fleets. What is also certain, is that the lockdown has changed the way people work and communicate, but opinions diverge as to the long-lasting effects.

In such uncharted territories, scenario planning can be a useful business tool. It models and assesses every possible outcome over a long period of time. It’s not a crystal ball, but it creates a series of alternative ‘what if’ scenarios, often extreme, against which the impact of future plans can be measured. Its aim is to spot weaknesses and prepare the ground for policies that are more resilient.

To help fleet decision makers stress-test future strategies, you could assess them against the following three what-if scenarios.

SCENARIO 1 – The Green Scenario

Companies emerge from coronavirus lockdown with a renewed commitment to environmental goals and find that access to financial support from the EU, national and local governments is closely linked to reducing carbon emissions.

Businesses start to ask how many professional business miles they really need.

Businesses downsize their fleet sizes, operating fewer vehicles and restricting them to essential journeys.

A massive Europe-wide expansion in renewable energy makes electricity a cheaper power source than petrol or diesel.

Employees have become used to cycling and walking to work during the lockdown, prompting authorities to prioritise road space for active travel.

More employees work from home, reducing the need for company cars.

Mobility as a Service becomes a key feature of employment contracts.

SCENARIO 2 – The Digital Scenario

Online society, online economy – the coronavirus lockdown prompts a fundamental shift in the way businesses and private individuals buy products and organise their corporate and personal life. Digital communication is all around. Shopping shifts online and delivery becomes central to the retail experience.

COVID-19 has forced fleet managers into a more pragmatic and decentralised fleet management with digital tools helping them to execute their role.

Retail space and location become less important than warehouse space and location.

Businesses need freight consolidation centres to gather packages prior to last mile delivery.

Logistics and delivery firms start to share warehouse and hub facilities.

On-demand mobility will grow as the need for professional miles will become more punctual rather than constant.

Punctual delivery times become a vital USP – customers expect to track deliveries minute-by-minute in real time.

SCENARIO 3 – The Cost Scenario

Cost cutting chaos – the economic impact of the coronavirus pandemic forces companies to adopt drastic cost-cutting measures.

Fleet renewal is suspended. Vehicle holding periods extend, contract mileages rise, service and maintenance challenges increase.

Perk company cars disappear from employment contracts.

Price becomes the most important factor in sourcing new vehicles, leading to a possible resurgence of diesel sales as oil prices remain low.

Fleets look to leverage their buying power through a single supplier – only a small number of OEMs have ranges capable of satisfying all fleet operational needs.

Long-term, fixed cost supply agreements become essential as fleets operate under strict budget controls during the corporate recovery.

After the recovery fleet managers will question if non-flexible, long-term solutions are the right choice.

AI and speech recognition allow for a natural and safer interaction with our car. Advanced connectivity also enables life-long updates and continuously improving skills, both to the benefit of the driver and the fleet manager.

1. Seat Leon: speaking your language

After “Hey Mercedes” and “Hello, BMW”, you probably expected the Spanish OEM to inaugurate “Ola, Seat” as a wake-up call for the infotainment system, but in fact, you just press a button to activate the voice recognition. It should recognise natural rather than strictly structured commands, allowing you to operate your Léon safer and more conveniently. Moreover, the embedded SIM means that the new Leon can be updated and offer new digital services throughout its lifetime. The app that comes with it enables you to monitor and manage your Leon remotely.

2. Land Rover Defender: two eSIMs are better than one

At CES 2020, JLR showcased a brand-new Defender featuring the world’s very first Twin LTE modem. What it actually means, is that this Land Rover can download Software-over-the-air (SOTA) updates on the move without interruption and while streaming music and apps, so without affecting the day-to-day connectivity. In addition, customers can connect two mobile devices to the infotainment at once using Bluetooth, so the driver and passenger can enjoy hands-free functionality concurrently without the need to swap connections. Finally, the dual eSIM allows the Defender to roam across multiple networks in different regions to optimise connectivity.

3. FCA: Uconnect 5 is future-proof with Android OS

Next to Volvo and Polestar, Fiat Chrysler Automobiles is also integrating Google’s Android Operating System in its infotainment unit, bringing access to a broad catalogue of applications. In planning for additional automated driving technology, the all-new Uconnect system comes with a Telematics Box Module (TBM) that assists in quickly moving large amounts of data. It’s 5G ready, too. Finally, with the available Uconnect app, which allows you to unlock and start the vehicle, FCA cars will be ready for sharing.

4. Mercedes-Benz in-car office: easy conf-calling

With the “In-Car Office” service, Mercedes drivers can access certain Office functions and important data directly in the car. For example, “In-Car Office” uses the location data in the calendar and automatically records it in the vehicle’s navigation system. In addition, the user can participate in a conference call without having to search for dial-up details. The system automatically recognises the required PIN code and uses it immediately. Drivers of an MBUX equipped Merc don’t have to lift so much as a finger: they can use the “Hey Mercedes” voice command function.

5. Android Auto comes to BMW – and its wireless People not belonging to the Apple community, rejoice: BMW has finally struck a deal with Google.

That means Android users can soon mirror their phone screens onto the central display of their Beemer and use messaging, navigation and music apps. Icing on the cake: the connection is wireless – no more fiddling with USB cables. Cherry on the icing: the phone’s data also appears in an adapted form in the instrument cluster’s info display as well as in the head-up display. Android Auto will be available from July 2020 for all vehicles with BMW Operating System 7.0.

The authors, Andreas Gissler, Andreas Quentin, André Gerhardy, Jan-Hendrik Bomke conducted a study called “Shared mobility: from ownership to on-demand” published in the paper “The Transforming Mobility Landscape” realized by Accenture in January 2020. In this study the authors explain how the consumption of mobility will change dramatically over the next 25 to 30 years and that the entire industries will be compelled to rethink their business models.

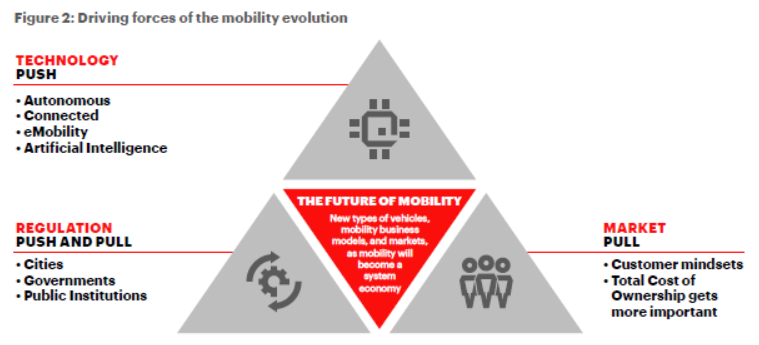

DRIVERS OF CHANGE

From how consumers expect to get around, to their perceptions of vehicles, to vehicle technology and design—everything about mobility will be dramatically different. The convergence of three key factors will be the driving force behind this change (Figure 2).

MARKET PULL

Consumers’ mindsets and behavior regarding cars are already substantially different from a decade ago and will continue to evolve over time, forcing companies to innovate to meet changing demands. In China, for example, more than 80 % of the population think that owning a car will be much less important and car sharing much more convenient. Similarly, consumers in Western countries believe that in the future, cars will no longer be seen as status symbols, and consumers will be more willing to use car sharing or even share their own car. Yet the full change to “as-a-service” business models will take time—it’s going to be an evolution rather than a revolution.

TECHNOLOGY PUSH

The proliferation of technological advancements is transforming the vehicle itself—from connected to electric to, ultimately, autonomous. The connected revolution is nearly complete: by 2025, all new vehicles will be connected vehicles, and 40 % of them will have embedded telematics, putting software at the center of the driver’s experience. By 2030, 30 % of all new vehicles will be electric. The true game changer comes by 2045, when half of newly sold cars will be partially or fully autonomous — which will have a massive impact on current consumption patterns by turning drivers into riders. As vehicles and their accompanying technologies evolve, they will continue to disrupt mobility-related industries, making possible entirely new business models and spurring even greater inventions.

REGULATION PUSH AND PULL

By 2050, about two-thirds of the global population will live in cities, more than double the figure in 1970.

Without government action, this will mean more cars and trucks on the streets, forcing commuters to spend more time in traffic jams and generating more pollution that threatens both people’s health and the environment. Regulators need to rethink how they address traffic to fulfill their mission to make worry- free and clean, sustainable mobility available to a city’s inhabitants. We’re already seeing cities taking steps to that end, such as new regulations to meet sustainability targets, additional tolls or fees for personal vehicles, and restrictions on goods delivery by trucks in the city center. As such actions become more widespread, they will create greater incentive for people and businesses to find ways other than driving their own vehicles to get around increasingly populous cities.

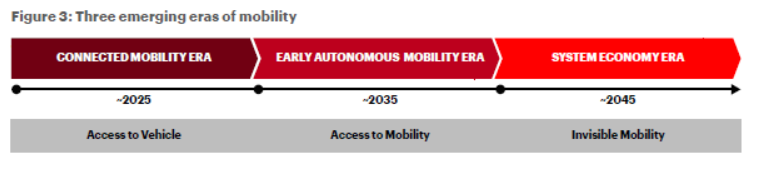

THREE ERAS OF MOBILITY

As the preceding forces evolve, we’ll see a corresponding evolution in mobility itself—embodied by three distinct eras (Figure 3).

CONNECTED MOBILITY ERA

In the first, the Connected Mobility Era, consumers still place a priority on access to vehicles themselves. However, these vehicles will grow increasingly intelligent, enabling new service models. Car sharing also will continue to expand, encouraged by government regulations to limit private cars and reduce congestion on city streets, as well as the more favorable economics of vehicle usage compared with ownership.

EARLY AUTONOMOUS MOBILITY ERA

As new autonomous vehicles become viable for the masses, we’ll enter the Early Autonomous Mobility Era, when consumers prefer access to mobility-as-a-service over access to a vehicle. Cities and public institutions, in turn, will have to respond by investing in their infrastructure and putting in place the right regulations to encourage the deployment of autonomous technology that boosts access to mobility.

SYSTEM ECONOMY ERA

When fully autonomous cars become commonplace, the System Economy Era begins to take shape. Through the emergence of various forms of mobility services, mobility moves to the background. Consumers will see mobility as a utility, available on-demand without much thought about how it happens—much like they view electricity in their homes today. In this era, cities and public institutions will have to fully regulate mobility to accommodate this “invisible” utility. Furthermore, automotive OEMs will need to adapt not only their marketing and sales strategies, but also the way vehicles are designed.

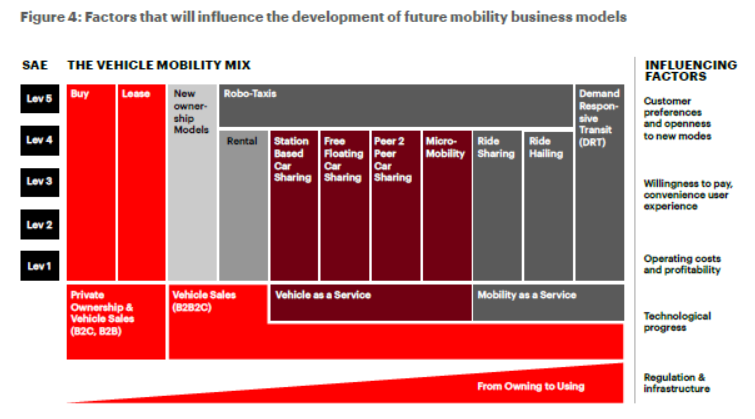

THE VEHICLE MOBILITY MIX AND INFLUENCING FACTORS

What does all this mean to the mobility ecosystem’s players and how they make money? To be sure, the mobility evolution will create massive challenges for traditional OEMs and their current business models. But it also opens up tremendous new opportunities, not to mention compelling new revenue streams for any company willing to think boldly about how and where it can play as these eras unfold.

In the future, companies will generate revenue from mobility in three primary ways:

Vehicle Sales: the traditional automotive business of designing, building, and selling cars to consumers and companies to satisfy long-term mobility needs

Vehicle-as-a-Service: the vehicle (such as cars, bikes, or scooters) is offered as-a-service to consumers to satisfy short- and mid-term mobility needs

Mobility-as-a-Service: mobility itself is offered as-a- service—whereby the consumer is no longer the driver, but the rider—to satisfy short- and mid-term mobility needs

When analyzing the respective development of each business model, one must consider five main influencing factors clustered around customers, the public sector, and mobility industry players (Figure 4).

From a customer perspective, three big factors will drive the choice of mobility mode: customers’ willingness to pay for mobility; the convenience they expect from the service; and other customer preferences, such as environmental values or desire for predictability. A general openness to new ways to get around also will be critical to the success of innovative new business models.

The public sector also plays a vital role in the future success of new forms of mobility. This includes delivering the required infrastructure (be it roads or 5G networks), creating the appropriate regulatory environment, and orchestrating the mobility mix in countries and cities (the last of which is also key to defining the availability and supply of mobility modes).

Last but not least are the mobility industry players, which will need to drive the technological progress needed to make new business models possible and to determine how to make those models profitable (which means operating cost management will be key to long-term business success).

Although each factor on its own can significantly influence mobility’s future, the interplay of all factors— as well as geographical and regional differences in customers and public sector players—will ultimately decide what tomorrow’s mobility mix actually looks like. The real game-changer will be autonomous technology. When autonomous vehicles reach Level 5—full automation—driverless cars will be able to operate on any road and in any conditions a human driver could negotiate. This will make robo-taxis technologically and, at some point, economically feasible, which could spell the end for other mobility services based on Vehicle-as-a-Service (VaaS) and Mobility-as-a-Service (MaaS) (Figure 4).

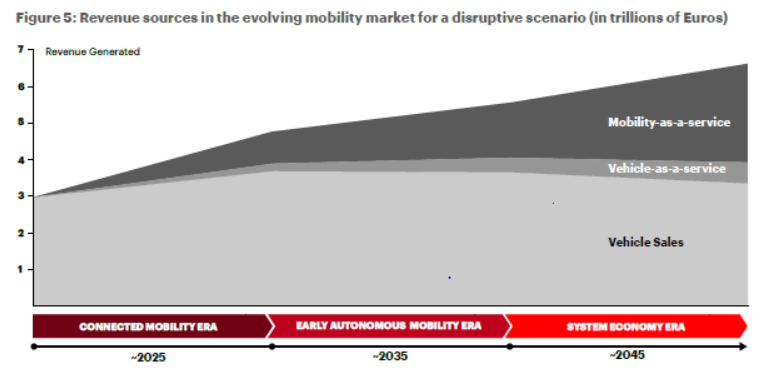

Let’s look in more detail at the three dominant types of business models we can expect to see in the coming years, how they’ll likely evolve, and their projected revenue trends over time (Figure 5).

VEHICLE SALES

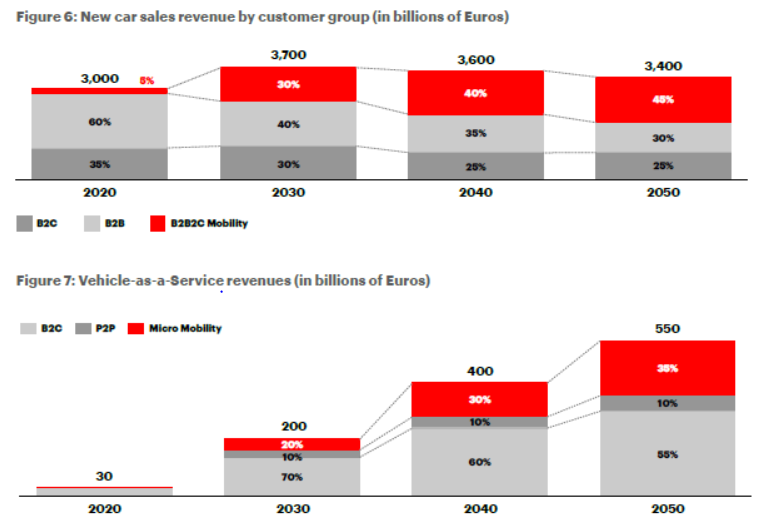

Regardless of the era, vehicles will still be needed and a business model that includes producing vehicles for sale will remain viable. In fact, vehicle sales will still account for the largest proportion of total revenue generated by mobility players across all three eras, and global new car sales will grow by 1.6 % annually until 2050, spurred by economic and global population growth. Revenues from new car sales also will increase throughout the Connected Era, peaking during the transition to the Early Autonomous Mobility Era (2030) before entering into a slow, gradual decline back in line with today’s figures.

However, the types of vehicles made, who buys them, and the revenue generated will certainly change (Figure 6). In 2050, vehicles will mainly be sold to corporate fleets and mobility fleet operators to provide short-, medium- and long-term mobility on-demand.

Privately owned vehicles will remain the primary mode of transportation in rural and suburban areas. Because they’ll be those consumers’ primary mode of transportation and will have greater comfort features and superior technology compared with vehicles used in fleets, they’ll likely command a premium price.

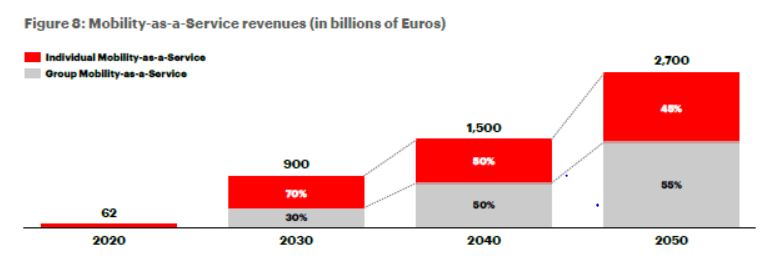

VEHICLE-AS-A-SERVICE (VaaS)

As connected vehicles become increasingly autonomous, VaaS will become increasingly popular. VaaS business models will emerge to provide vehicles and the necessary infrastructure to flexibly book and share vehicles that fulfill short- and medium-term mobility needs. The most prominent of these business models will be business-to-consumer (B2C) car sharing and micro-mobility (akin to today’s electric scooters), with people-to-people (P2P) car sharing playing a minor role due to people’s reluctance to let strangers drive their vehicles.

However, despite strong growth between 2020 and 2040, VaaS will only play a minor role in the new mobility environment (accounting for less than 10 % in 2050) (Figure 7). Among the factors that will impede further growth of VaaS are asset-heavy operations within B2C car sharing, lack of trust between P2P car sharing members, high turnover needs in micro- mobility, high operations and insurance costs, overall regulation, and a general difficulty in scaling. Hence, VaaS can be characterized as a transition stage toward full-fledged mobility-as-a-service (MaaS) offerings and, importantly, a big step toward getting consumers more familiar with and confident in mobility services.

MOBILITY-AS-A-SERVICE (MaaS)

MaaS business models will disrupt and transform the way people consume mobility—becoming the option of choice for short-term mobility needs, turning drivers into riders, and effectively relegating mobility to the background by making it a passive rather than active pursuit. MaaS will come in two “options”: Individual MaaS will include initial business models such as ride hailing, which eventually will give way to the more economical “robo-taxis.” Group MaaS will be primarily focused on-demand-responsive transit, whose value proposition is effectively and efficiently organizing ride pooling and which, with effective partnering, can serve as a complement to or even replace existing public transportation networks.

As MaaS becomes more prevalent, the revenue it generates will grow accordingly—increasing more than fortyfold between 2020 and 2050 (Figure 7), when it will comprise 40 % of the mobility industry’s total revenues. The MaaS market will be characterized by a high degree of development and be highly dependent on technology advancements and regulation. For instance, fully autonomous driving will be key to driving down MaaS’s marginal costs, enabling cost and price leaders to dominate the market.

KEY TAKEAWAYS

The future mobility ecosystem and value chain will reshuffle the deck for everyone involved, as disruptive new players enter the market and mobility service providers, cities, and other stakeholders will shift the balance of power and key strategic control points across the ecosystem. In that context alliances and strategic partnerships are necessary, to generate critical mass to scale mobility services in a very short time.

Until now the mobility ecosystem has mostly failed to generate sustainable profits because of customers’ unwillingness to pay and high operational and financial costs. As a result, a clear “separation of duties” is necessary among vehicle manufacturers (which should run their mobility efforts apart from their traditional car-making business); suppliers (such as fleet operators); and the mobility providers themselves to build the right set of capabilities and resources to given the severe competition. Doing so will be critical to reducing marginal costs, optimizing asset utilization, building the right product offering, and generating sustainable profits.

When it comes to scaling mobility offerings, the mobility ecosystem not only faces operational and regulatory barriers, but also highly differentiated and diverse customer demands. Customer expectations for how they actually will consume mobility differs significantly across continents, countries, and regions, which leads to significant offering and operational complexity. Therefore, the mobility ecosystem must, first and foremost, take a regional or local approach to be able to deliver the services customers want.

While scaling businesses to minimize costs and reach a critical mass is central to all mobility providers, regulators will be called on to regulate and orchestrate mobility offerings across cities to create an environment in which mobility can grow sustainably. Determining and supporting the right mixture of mobility offerings will be key to giving residents access to new forms of mobility, managing competition, and learning how to best organize new forms of transportation.

Last but not least, the mobility revolution is only possible if all stakeholders can build the necessary infrastructure that, for example, enables the use of connected and autonomous vehicles at scale and efficient mobility operations. This, in turn, hinges on regional orchestration and collaboration, as well as significant public investments.

After a period of new market launches and expansion, several carsharing services are downsizing or even discontinuing their operations altogether. What will the carsharing industry of the future look like?

Earlier, GM ended Maven, a carsharing service in North America. Book by Cadillac was suspended at the end of 2018 with a new programme set to launch in early 2020.

Deep pockets

Yves Helven, Global Fleet expert, believes Cadillac was not helped by its traditional customer base, which is older and more conservative.

Building a successful carsharing service is no easy feat, he said. “First of all, you need a very customer-friendly, easy to use platform. Secondly, you need good buy-back deals with carmakers. And you need backers with deep pockets, because it’s very hard to make money in this industry.”

Philippe Bismut, Fleet Europe expert and formerly CEO at Arval, agrees. “I don’t know of one carsharing company that is making money, even more so if it’s a free-floating business. To me, the carsharing solutions that are successful are the ones that are based on existing corporate fleets or within a dealership, where some of the costs are already being absorbed elsewhere.”

Peer-to-peer

Pascal Serres, Fleet Europe expert and formerly deputy CEO at ALD, also sees potential in peer-to-peer platforms. “A peer-to-peer business in less expensive in terms of capital as they don’t need to fund the vehicles. Other businesses are much more difficult although programmes backed by OEMs also have their place in the market.”

Mr Helven agrees there is a place in the market for peer-to-peer carsharing, adding we should keep an eye out on what Tesla’s planning to do. “In early 2019, Tesla launched an over-the-air update to prepare all Teslas for carsharing. This feature hasn’t been activated yet but once it is, all Tesla owners will have the option to offer their vehicle on a peer-to-peer carsharing platform. I believe Tesla could attract the right customers for such a service and Tesla could make it work.”

Shared Teslas?

“At a later stage, Tesla could set up its own carsharing service built on this peer-to-peer experience. They might even build a dedicated small city car for this service, in which they could reuse batteries of old Teslas, enabling them to build a true closed ecosytem.”

All three experts agree carsharing is here to stay. Don’t remove it from your MaaS menu yet, but be prepared to change suppliers. “There will be a high turnover in the sector,” concluded Mr Bismut.

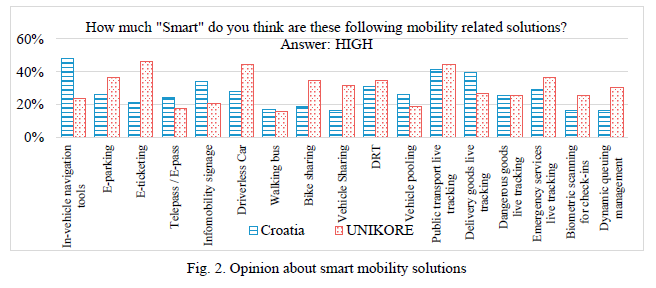

Researchers Sanja Surdonja, and Aleksandra Deluka-Tibljas, from the Faculty of Civil Engineering, University of Rijeka, Croatia and Tullio Giuffre from Università degli Studi di Enna “Kore”,Cittadella Universitaria, Enna, Italy, presented an article at the International Congress on Transport Infrastructure and Systems in a changing world (Rome, September 2019), regarding Smart Mobility Solutions.

1. Smart mobility

Sustainable management of urban areas has become, during the last decades, one of the most important challenges of the 21st century that resulted in the concept of “smart city”. Smart City includes different aspects of city management: building, energy, environment, government, living, education and mobility.

Smart Mobility is often highlighted as a key system without which the Smart City could not be sustainable. A number of smart solutions have been analyzed and implemented in the context of smart mobility/movement in the cities and beyond. Many of these solutions are based on IT and they include a vehicle navigation system, e-parking, e-ticket, info-mobility signalization, demand-responsive transport, car sharing, bike sharing, public transport live tracking but also some innovative solutions are not necessarily related to IT (walking bus).

From the other hand, Intelligent Transportation Systems (ITS) were already introduced in the cities as a solution to mitigate traffic congestion and to reduce pollution by enhancing smart mobility, fuel efficiency, accessibility, and safety. ITS can produce benefits related to traffic congestion and air quality without foreseeing the construction of additional roads or transport infrastructures.

They are variegated and include several different technologies and software solutions such as advanced traffic management systems (e.g., freeway and incident management systems, electronic toll collection), advanced traveler information systems (e.g., dynamic message signs, in-car real-time traffic information and navigation systems), advanced public transportation systems, commercial vehicle operations and so on.

According to Debnath, in order to consider that the mobility system of a city is smart, it is necessary that it is self-operating and self-correcting and requiring little or no human intervention. The main aspect of smart mobility is connectivity; thanks to connectivity and big and open data, users can transmit all the traffic information in real-time, and public administrators can simultaneously conduct dynamic management.

Data related to mobility may change constantly (e.g., data on available parking spaces, traffic conditions, accidents, train or bus delays), and may be communicated immediately to the mobile app users, to ensure a smart, easy, and smooth trip.

The introduction of new transport systems and services, on the one hand, leads to an evolution in the demand for transportation, and on the other hand, it is also able to change user’s behavior. For this reason, it is important to develop advanced tools and methods for investigating the characteristics of mobility demand.

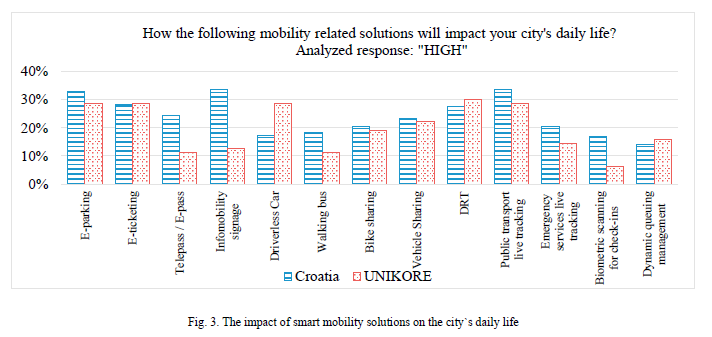

2. Smart mobility survey

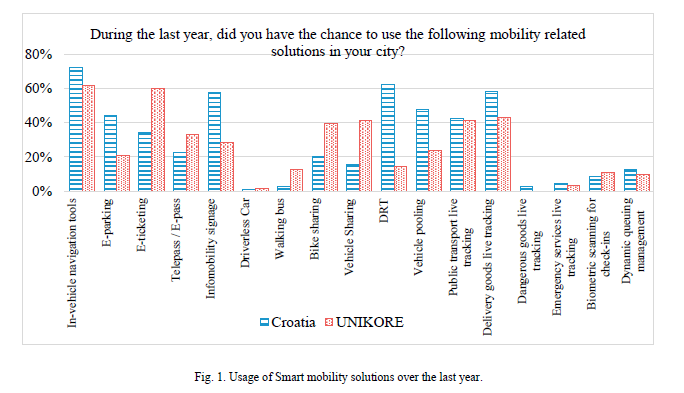

The researchers explain that the Smart Mobility Survey has been conducted in Croatia, in 2017, with the aim to establish users opinion on a number of the different, mostly ICT supported, solutions that have been lately used in the world (and Croatia) for enhancement of mobility in the cities.

The survey has examined the familiarity with such solutions, the current level of their use, and future expectations of using existing and new smart solutions (e.g. autonomous cars) in everyday life. Almost a third of the sample stated that real-time information about public transportation, e-parking, and e-ticketing for transportation services are the most impactful solutions for their city ́s daily life.

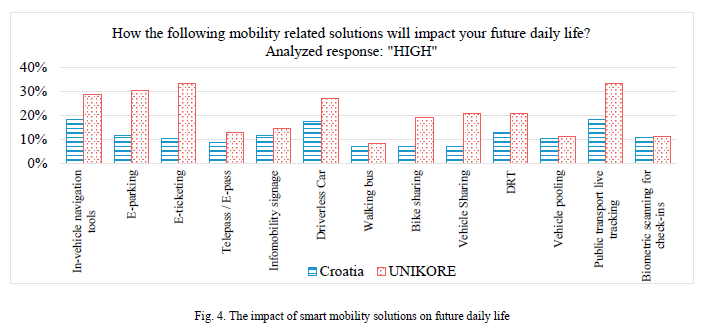

However, in the case of impact on the future daily life, in Croatian survey, respondents highlighted just a few of the smart mobility solutions as significant: in-vehicle navigation tools, driverless car, and public transport live tracking.

3. Driverless cars – a near future mobility solution

The authors also highlight that recent studies display a positive picture of the public opinion on fully automated driving. Nevertheless, a non-negligible level of the reluctance of the potential users is also partly present. A research done by Schoettle & Sivak investigated the public opinion about automated and self-driving vehicles in the US, the UK, and Australia.

Although 57% of the respondents had an overall positive the results showed concern about riding in completely self-driving vehicles.

Conclusions

Smart mobility as an important part of the Smart City concept includes different smart mobility solutions of which some are already present in our cities (e.g. e-ticketing, e-parking, live-tracking, etc.) and some are in a testing phase like driverless cars.

The survey has shown that mobility solutions, already in use, are expected to have the highest impact on their everyday life in the future. Unexpectedly, young responders (20-30y) represent a major part of the “skeptic” among the population included in the survey.

The researchers stress that it is important to have a more public debate (presentations, surveys, education…) of future mobility solutions and their benefits so that they become more acceptable to the wider population.

According to the authors the next goal should be to stay ahead of the gradient of change valuing some practical implications of the new approach. Indeed, it should be needed an advanced and detailed technical framework in order to shape the mobility demand and its behavior referring to future transportation solutions.

Researchers

Sheila Tricia Guedes Pastana, Glauber Ruan Barbosa Pereira, Kleber Cavalcanti

Nóbrega and Domingos Fernandes Campos from the Potiguar University of Nata,

Brasil, published an article on Rebrae (Revista Brasileira de Estratégia),

regarding sustainable urban mobility. The article provides an a-up to date

review on this issue. Here there are some of the key issues.

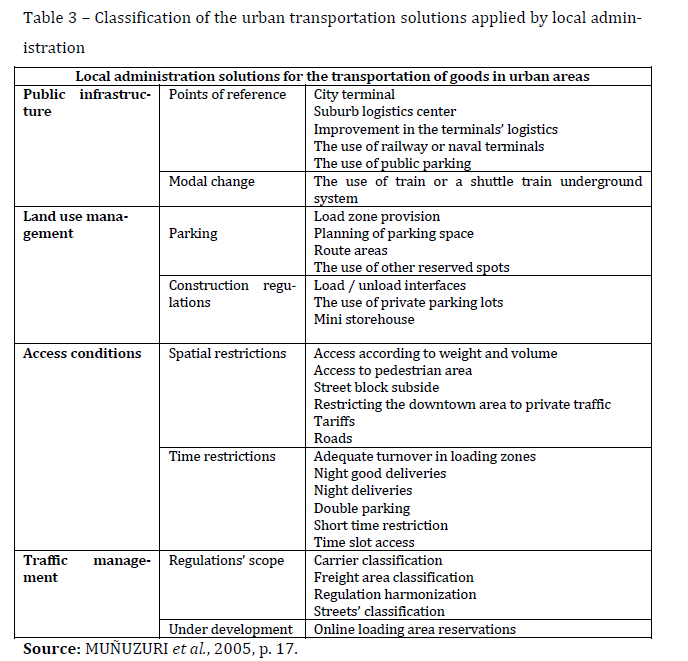

Urban logistics is present in citizens’ daily life all over the country since it also deals with the displacement of goods and people in the cities, with the flow of several means of transportation, and with the interaction and the integration with private and public organizations.

Thus, the authors explain that this study focuses on urban logistics and sustainable mobility, which is present in urban spaces.

Nowadays, the issue about population growth, about urban settlement with no adequate planning, dangerous traffic jams and environmental and social unsustainability has fostered concerns about the search for a new city model, one that can get several denominations, such as intelligent mobility and intelligent city.

There

is currently the concept of intelligent mobility, which comprises two moments:

the first one focuses on information technology as a way to improve urban

transportation planning; the second one incorporates people and consumers as

important actors in this process.

The

researchers highlight that both integrated moments, such as technology and

consumers, contribute to the improvement of intelligent mobility.

Urban Logistics

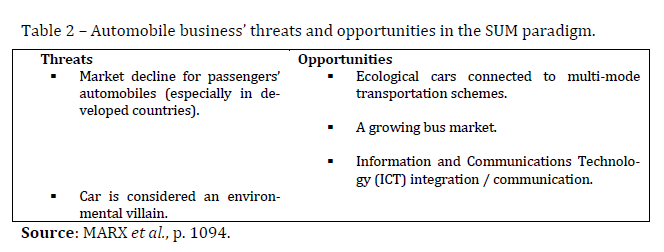

In the last century, vehicles played a leading role in urban logistics as symbols of development and status, both for the transportation of goods and of people. Upon transporting people, the automobile favored the agility, comfort, convenience, more independence, among others. Upon transporting goods, automobiles brought in more swiftness, access to several places, market expansion, and more profitability, among others.

Problems from this model of mobility also came along, such as pollution, traffic jams, accidents and traffic casualties, noise disturbances, social exclusion, global warm-ing, among others.

Thus,

in the current century, although automobiles are still very useful and the most

popular mean of transportation in the world, several countries see them as an

environmental villain.

In

this context, the authors understand that the logistics developed by a city can

be defined as the process of optimization of the urban logistics activities,

taking into account the social, environmental, economic, financial and energy

impacts of the urban freight movement.

The urban logistics objective is the global optimization of the urban logistics system, considering costs and benefits of a certain plan of action for the public and private sectors, encompassing planning, implementation, and efficient flow control and storage of related goods and information, on an urban scale.

Innovative strategies in the planning

of sustainable urban mobility

On

urban mobility, the research refers to

L. Machado who mentions the European Union’s understanding, which states

how important and urgent it is to rethink the current model by optimizing and

using other types of transportation, “organizing the inter-modality between

different means of collective transportation (train, electric, subway, bus,

taxi) and individual transportation (automobile, motorized, bicycle, on-foot

travel)”, envisioning the triple bottom line balance.

As

for intelligent mobility, the study also refers to Garau, who considers that it

is not possible to dissociate it from sustainable mobility, for there is no use

in having only one system of intelligent traffic; it is necessary to invest in

less polluting means of transportation, to reduce accidents and traffic jams,

in continuous and safe bike lanes, to improve the individual mobility, to

reduce the commuting time, and to favor the access to information, among

others.

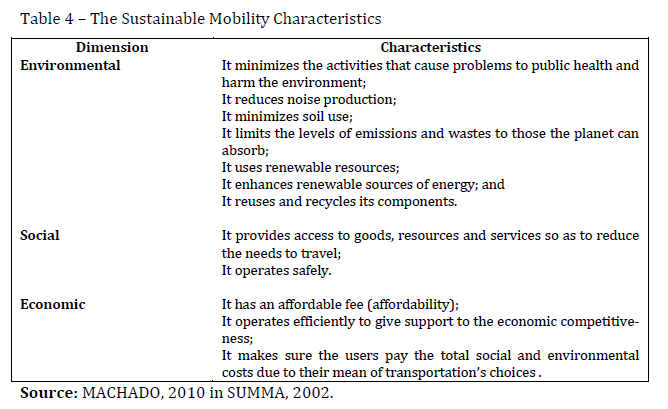

In the meantime, the adoption of practices that cover the set of sustainability in its environmental, social and economic dimensions will favor the sustainable mobility and, on the other hand, will demand investments, an efficient management, and the breakdown of paradigms and a change of attitude.

The researchers highlight that the sustainable planning of transportations will demand mental changes so as to design the planning and the practices, the funding, the broad and detailed analysis of the impacts, as well as the comprehension of the needs of the parties involved.

Final considerations

Regarding the sustainable urban mobility, and based on the review analysis of the literature here developed, there is still no common ground about the concept of sustainable urban mobility, but it is true that if nothing is done in time, the quality of life in urban spaces in the cities will be unsustainable.

As

observed along this research, it is important to develop strategies that

involve planning, innovation and urban mobility management, so as to ensure the

sustainability of life, relationships and businesses in the cities.

The

authors stress that the challenges to achieving sustainable mobility are

complex, since they involve changes in the way of thinking, innovation

strategies, and using and planning urban logistics. Several decisions will

probably displease some stakeholders, such as the possibility to design

measures to restrict the use of private saloon cars, among others.

These

decisions will play a considerable role for the public managers and might

trigger a political burden for the implementation of decisions which favor the

public welfare and the community usually displeases some stakeholders.

Become

a Contributor!

We’re always looking for interesting ideas and content to share within our community.

Get in touch and send your proposal to: press@octotelematics.com

Your privacy

This site uses cookies or similar technologies of a technical nature, including from third parties (to allow the website to function correctly and smoothly), and, with your consent, also profiling (to send advertising messages in line with your preferences expressed in the context of web browsing and/or to analyze the behavior of visitors to the site), as specified in the Cookie policy. You can manage your preferences using the 'Cookies Settings' button. We remind you that clicking on 'Reject all cookies' or closing the banner using the appropriate X, involves the persistence of default settings, and therefore you will continue to navigate in the absence of cookies other than technical ones.

Privacy Preference Center

General information

When you visit any website, it may store information on your browser, mostly in the form of cookies. This information might be about the site navigation, your preferences or data relating to the device used. Some of these cookies are used to provide you with a better browsing experience and allow you some features (Navigation or session cookies, Functionality cookies, Analytics cookies), others to send you personalized advertisements (Profiling cookies). You can choose not to allow the installation of cookies - net of the technical ones necessary for the functioning of the Site - by clicking on the headings of the relevant categories to find out more and change the settings using the "ACTIVE/INACTIVE" slider. However, disabling certain types of cookies may limit your browsing experience on the Site and the services we can offer. Octo informs users that the different types of cookies used have a persistent duration until the cookie configuration settings are changed.

Technical Cookies

Always on

The technical cookies used by Octo are necessary for the functioning of this Site. This type of cookie is used in response to user requests for services, such as authentication to access restricted areas or filling in forms. These cookies ensure the normal navigation and use of the Site. You can set the browser used for navigation to block these cookies, but some sections of the Site may not work.

Octo telematics

pll_language - www.octotelematics.com

The cookie stores the language code of the last page visited. (duration: 1 year)

PHPSESSID - www.octotelematics.com

The cookie is used to store and identify a user's unique session ID for the purpose of managing the user's session on the website. The cookie is a session cookie and is deleted when you close all browser windows. (duration: Session)

YouTube

VISITOR_INFO1_LIVE - *.youtube.com

Used to track the information of YouTube videos embedded on a website. (duration: 5 months and 27 days)

CONSENT - *.youtube.com

(duration: 16 year and 8 months)

YSC - *.youtube.com

It is used to track the views of embedded videos. (duration: Session)

Analytics Cookies

Octo uses analytics services to understand the level of effectiveness of the content, the interests of users and to improve the functioning of this Site.

Google

test_cookie - *.doubleclick.net

The purpose of the cookie is to determine whether the user's browser supports cookies. (duration: 15 minutes)

IDE - *.doubleclick.net

It stores information about how the user uses the website and any other advertisements before visiting the website. It is used to present users with advertisements that are relevant to them based on their user profile. (duration: 1 year and 24 days)

Profiling Cookies

This Site uses Profiling cookies to send targeted advertising to users, that is in line with their preferences expressed during navigation. In particular, these types of cookies are installed by third parties, advertising partners of Octo Telematics S.p.A. who may present, also on other sites, ads and advertising content based on the interests shown. The installation and use of these cookies requires the user's consent.

Facebook

_fbp - *.facebook.com

It is used to deliver advertisements when they are on Facebook or on a digital platform powered by Facebook advertising after visiting this website. (duration: 90 days)

fr - *.facebook.com

It is used to show relevant ads to users and measure and improve ads. The cookie also tracks user behavior across the web on sites that have Facebook pixels or Facebook social plugins. (duration: 90 days)

datr - *.facebook.com

The purpose of the cookie is to identify the web browser used to connect to Facebook regardless of the user who is logged in. This cookie plays a key role in the security and integrity features of the Facebook site. (duration: 2 years)

LinkedIn

lang - ads.linkedin.com

This cookie is used to store a user's language preferences to offer content in that stored language the next time the user visits the website. (duration: Session)

bcookie - *.linkedin.com

The purpose of the cookie is to enable LinkedIn features on the page. (duration: 2 years)

bscookie - www.linkedin.com

This cookie is a browser cookie ID set by the linked share buttons and advertisements tags. (duration: 2 years)

lidc - *.linkedin.com

Used for routing. (duration: 1 day)

li_gc - *.linkedin.com

Used to store the consent of users of the Site regarding the use of cookies other than technical ones. (duration: 2 years)

UserMatchHistory - *.linkedin.com

Used for LinkedIn Ads ID synchronization. (duration: 30 days)

AnalyticsSyncHistory - *.linkedin.com

Used to store information about the time when a synchronization with the lms_analytics cookie took place for users in the designated countries. (duration: 30 days)

Vimeo

vuid - *.vimeo.com

This cookie is used by Vimeo to collect tracking information. It sets a unique ID to embed videos in your website. (duration: 2 years)